Background screening in the United States is a common practice and hence that explains the plentiful number of background screening vendors. However, the regulatory requirements can be complex. Avvanz, a global multi-award backgrounds screening company with capability to conduct more than 20 types if checks across 150+ countries including the Americas is here to support clients in meeting these complex regulatory requirements.

The FCRA

The Fair Credit Reporting Act (https://www.ftc.gov/legal-library/browse/statutes/fair- credit-reporting-act), or FCRA, is a US federal law regulating several aspects of the consumer reporting industry. The FCRA is not just limited to governing credit reports; it also governs information provided by background screening companies for broader information provided, as well as companies that use their services. It aims to ensure the fairness of the information recorded in consumer’s files and used with these entities. Predominant in the FCRA is the term “consumer report”. A consumer report is more than a credit report. It is a report from a Consumer Reporting Agency (“CRA”) that provides information on an individual’s credit history, character, reputation. Such a report would be used to determining this person’s eligibility for

(A) credit or insurance to be used primarily for personal, family, or household

purposes;

(B) employment purposes; or

(C) any other purpose authorized under section 604 [§1681b] of the FCRA.

Whether you are screening for employment purposes, gig economy, tenant screening,

or board memberships, these activities will often fall under the requirements of the

FCRA.

FCRA and Background Checks

The FCRA has a significant impact on background screening because background checks involve collection and use of consumer credit information and employers use background checks to assess the suitability of job candidates, tenants and other individuals. These background checks can include information about a person’s criminal history, employment history, education and credit history. More information can be found here:https://www.avvanz.com/background-checks/

The FCRA imposes specific duties on users of consumer reports such as employers and

other entities. It also imposes duties on entities involved in producing consumer reports,

such as background screeners or the furnishers of information. These requirements include:

specific language for the notice and authorization of the background screen

notification to the consumer when potential adverse action will occur based upon the information found in the background screening report, and notification when such adverse action will occur

the ability of the consumer to dispute information provided in the consumer report

the ability of the consumer to obtain information from organizations about what information is held on them

In addition to the FCRA, other regulations, such as “Ban the Box” regulations and restrictions on the use of credit and criminal record reports, may govern the use of background screening information in decision making for an individual user. The requirements are complex and advice from legal counsel is advised.

In a nutshell, FCRA sets important standards for the collection, use, and sharing of consumer credit information in the context of background screening. Companies that perform background checks must comply with these requirements to ensure that their practices are fair, accurate and respectful of consumers’ rights.

How can Avvanz help?

When outsourcing your background checks to a provider, it is crucial that you work with a provider who is knowledgeable about the various US regulations, like Avvanz.

To support clients with their compliance requirements, we assist with:

background screening instructions and forms to help maximize client’s compliance requirements

information state and local requirements and summarizes of key issues facing effective and compliant background screening programs

easy to use portal (Avvanz ScreenGlobal) providing o client specific disclosure and authorization documents, allowing consumers to

digitally sign the documents o mechanism to send pre-adverse and adverse action notices to consumers

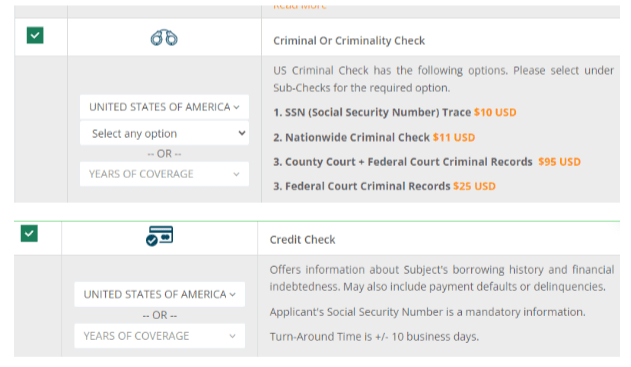

Providing applicant with final notice of adverse action Example screenshots (Showing List Prices before Discounts):

Should you need more information, feel free to drop a note at consult@avvanz.com.